Detalles

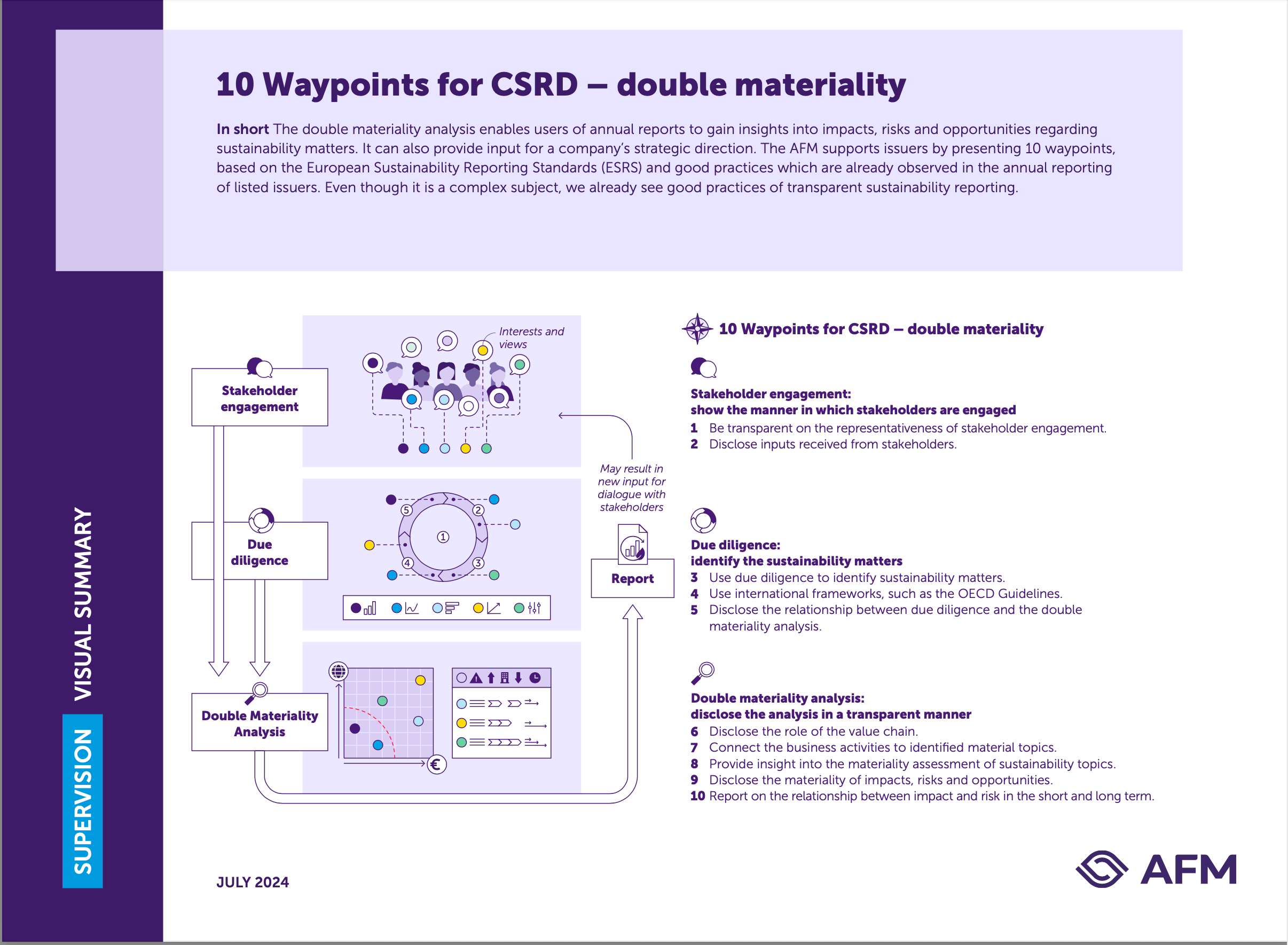

| Dual materiality analysis plays a key role in the Corporate Sustainability Reporting Directive (CSRD ) that came into force for large listed companies in 2024. Dual materiality analysis plays a key role in this regard. This analysis makes clear the effect a company has on the outside world (impact materiality) and how sustainability issues can impact a company's well-being (financial materiality). Information is material when its omission or misrepresentation may influence the decision-making of the user of the sustainability information. Understandable and transparent communication about dual materiality is essential, because it is the cornerstone of adequate sustainability information. This AMF study provides 10 benchmarks that anyone can benefit from when performing or using dual materiality analysis. |

Recursos relacionados

The Future for Nature in Transition Planning

The climate and nature crises are interlinked: climate change is the third leading cause of nature loss, with natural ecosystems…

Green and Sustainable Product Framework 5.0

Version 5.0 of Standard Chartered Bank's "Green and Sustainable Product Framework 2023" outlines the bank's approach, products and processes framed…

Pilots for the implementation of the TNFD LEAP approach in finance, infrastructure and the food sector

The TNFD has developed a series of recommendations and guidelines for organizations to identify, assess, manage and, where appropriate, disclose…